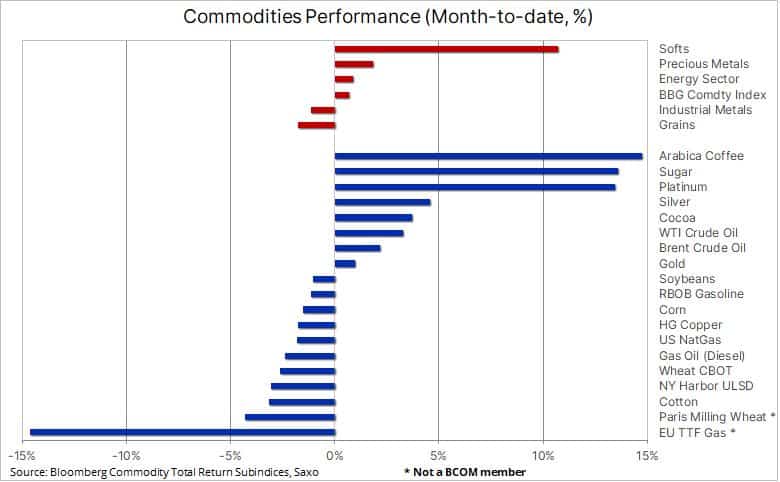

DUBAI, UAE — The commodity sector, following a strong start to the month – courtesy of an OPEC+ production cut supporting energy and lower US rate expectations supporting precious metals – has been drifting lower in response to ongoing concerns that economic weakness in the US and Europe may offset the positive impact of a recovering China. The Bloomberg Commodity Total Return Index, which is replicated by several major ETFs, an example here, and tracks 24 major commodity futures spread evenly between energy, metals and agriculture, trades close to unchanged on the month and down 5 percent on the year.

Apart from now fading gains in precious metals and energy, the index has been lifted by a strong month across soft commodities led by coffee and sugar. Both trading sharply higher in response to supply worries from major producers in Asia and South America. Raw sugar futures in New York trades near an 11-year high, above 25 cents per pound following lackluster crops in India and Thailand – two major exporters of the sweetener – helping drive global inventories to a decade-low.

Crude oil drops

Crude oil prices were heading for its biggest weekly loss since last month’s banking turmoil-led sell-off and, in the process, most of the gains that followed the OPEC+ production cut announcement on April 2 has now been wiped out. This renewed weakness is being driven by a combination softness in US economic data as well as lower gasoline and diesel margins pointing to softer fundamentals. Developments that have forced traders to reduce longs that were bought following the production cut announcement, the bulk of which were around $84.50 in Brent and $80 in WTI.

The weakness has also been supported by technical selling from traders looking to close the gaps that were left when prices opened sharply higher on April 3, in Brent to $80 and $75.70 in WTI. The big question now remains whether these levels, if met, can hold as it otherwise may trigger additional short-term focused momentum selling, thereby potentially forcing additional defensive actions from OPEC.

Overall, it has been a couple of challenging months for traders with the market whipsawing, first from the banking crisis, then OPEC+ production cuts and now continued worries about the risk of recession and its impact on demand. A concern that is currently playing in the refined product market where margins are under pressure across all the major regions. The weakness is being led by diesel, which powers heavy machinery, such as truck and construction equipment. Lower refinery margins into the peak demand season may lead to lower refinery demand and with that lower demand for crude oil.

Saxo keeps the view that Brent looks set to continue trading in the $80’s for the near future while we wait for the expected, albeit reduced, pickup in demand during the second half – as projected and reiterated by OPEC, IEA and the EIA in their latest oil market reports. A development that will likely boost prices and aggravate an emerging supply deficit in 2H23. However, the recovery in demand is still very uneven with China and a pickup in airline travel accounting for the bulk of the expected increase.

Gold, silver consolidate

After recently reaching a fresh cycle high at $2048/oz, just 22 dollars below the 2022 record peak, gold traders’ attention this past week turned to consolidation with the yellow metal drifting back below $2000. Having jumped by 13 percent since early March when the banking crisis triggered a major change in the outlook for US short-term rates, a correction was long overdue. Silver also encountered some profit taking after surging 31 percent since early March to reach a one-year high above $26/oz.

Looking at the recent dollar weakness and movements in 10-year real yields, it is clear how strong the rally in gold and silver has been, with the normal negative correlations to dollar and yields not explaining the move higher in both. Instead, last month’s main driver was the banking crisis which triggered a major change in the market’s expectations for the direction of US fed funds, from further hikes to aggressive cuts before yearend.

The drop in yields, now partly reversing, helped trigger the first sustained pick-up in demand from financial market participants such as private investors and asset managers via ETFs. Having been net sellers of exchange-traded funds backed by bullion for the past 11 months, these investors finally saw enough momentum in gold and evidence of trouble elsewhere to tentatively start giving gold a bigger allocation. However, this important investor group has not yet engaged in gold on a level that would seriously push the market higher. Having been net sellers of 465 tons between April 2022 until the banking crisis started last month, total holdings have only managed a 50-ton increase since then.

Speculators in COMEX gold futures also responded to the positive price momentum last month by starting the strongest four-week buying spree since mid-2019. During that period, the net long jumped 121k lots or 12.1 million ounces and with the market now consolidation some of these recently established longs are being reduced.

While the short-term outlook points to consolidation and the risk of lower prices, Saxo maintains an overall bullish outlook for investment metals, driven among others by the following developments and expectations:

Weakening dollar

Peak Fed rates, when confirmed, have historically on the three previous occasions during the past 20 years supported strong gains in gold in the months and quarters that followed

Central bank demand look set to continue as the de-dollarization focus continues to attract demand from several central banks. One unknown is how price sensitive, if at all, this demand will be. We suspect it will be limited, with higher prices not necessarily preventing continued accumulation.

We believe inflation is going to be much stickier with market expectations for a drop back to 2.5 percent being met in the short-term but not in the long-term, forcing a gold supportive repricing of real yields lower.

Geopolitical scene

Low ETF investor participation adding support should the above-mentioned drivers eventually provide the expected breakout.

Having rallied by close to 240 dollars since March 8, the short-term gold market focus has turned to consolidation with the risk of long liquidation from recently established longs weighing on the market. The loss of momentum signalled by the break below the 21-DMA, currently at $1995, may trigger a deeper correction towards the $1955-60 area.

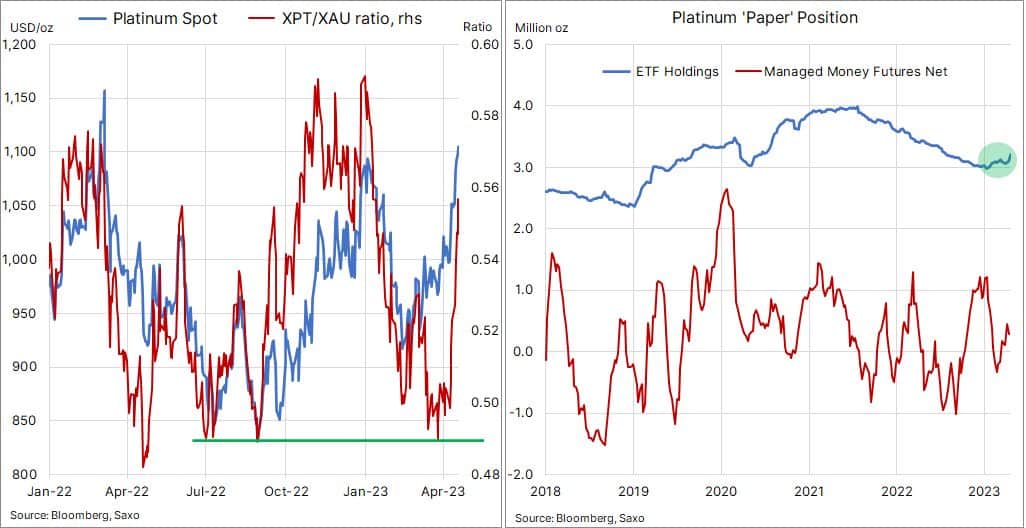

Platinum surge

The metal that has performed the best during the latest correction phase is platinum, which is utilised in catalytic converters, green hydrogen technologies, jewellery and investment demand. Over the past month, particularly this past week, platinum has narrowed its gap to gold by more than 140 dollars, with the rally being strengthened by the Friday break above resistance-turned-support at $1100 per ounce. In terms of investment perspective, traders often monitor the ratios between metals to evaluate relative value.

Last month, the Platinum/Gold ratio dropped to support at 0.49, a level from where relative platinum strength had emerged on three previous occasions during the past year, before rising to the current 0.555, reflecting a 13 percent outperformance.

As the gold correction unfolded last week, platinum remained supported due to supply concerns from South Africa facing frequent power disruptions and Russia. Additionally, the World Platinum Investment Council has highlighted that the white metal is under-owned by investors and speculators. During the recent surge in prices, gold attracted 114k lots of speculative buying during a five-week period to April 11, while platinum traders bought 9k lots and barely managed to turn a net short into a small 5.6k lots net-long.

Additional strength will be determined by platinum’s ability to hold above $1100 and whether it will continue to attract demand via ETF’s which jumped the most in three years this week to 3.2 million ounces, an eight-month high, the latter being a prerequisite for pushing the market towards a price supportive supply deficit.

European gas

European benchmark gas trades near a cycle low at €40/MWh ($13/MMBtu) with focus on weak demand and storage levels at 57 percent full being about 20 percent higher than usual for this time of year. Imports of LNG may hit a record in the coming weeks as US export continues to rise and competition from other buyers around the world remains muted.

During the past week, an average 14.3 billion cubic feet of gas flowed daily to US export terminals, an 18.4 percent year-on-year increase. The combination of these developments has left the market wondering whether EU storage sites can be filled before September – a development that potentially could send spot prices even lower.

However, so far the winter 2023/24 gas price which covers the period from October to March next year has yet to turn decisively lower, still trading around €55/MWh. A sign the market is not entirely comfortable about sending prices lower, primarily on expectations for a normal winter that would trigger higher demand than the recent one.

Copper trades lower

Mining companies’ quarterly results are continuing to roll in, and they highlight that global tightness in the copper market will continue at a time when copper consumption continues to rise, with the green energy transition driving demand from electrical vehicles, renewable power generation, energy storage and transmission. BHP reported a 12 percent rise in copper production for its nine-month reporting period, while keeping its production guidance for the year unchanged.

Rio Tinto meanwhile cut its outlook for copper production due to technical problems at two mines, and Chilean copper production giant, Codelco reported first-quarter output being at the lower end of annual guidance and expects output to stay at similar levels through next year.

Despite expectations that long term supply will struggle to keep pace with demand as the mention green energy transition gathers momentum, the short-term outlook for copper points to continued rangebound trading as these supporting factors are being offset by recession concerns following a week of softer than expected economic data. The High Grade and LME copper futures traded lower in response to these developments with HGc1 returning to the center of its current $3.8 to $4.2 range.

Ole S Hansen is the Head of Commodity Strategy at Saxo Bank.

The opinions expressed are those of the author and may not reflect the editorial policy or an official position held by TRENDS.