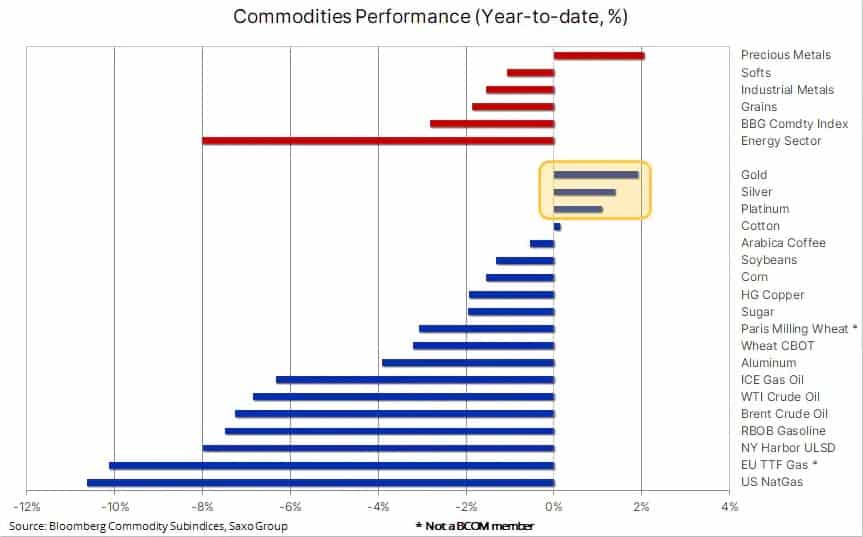

Gold together with silver and platinum are among the few commodities trading up as a new year gets under way. Gold’s newfound resilience and momentum from December has been carried over to January as investors seek shelter from what has been forecast to be another challenging year, especially for those with exposure to equities.

In general, we are looking for a price friendly 2023 for investment metals supported by recession and stock market valuation risks, an eventual peak in central bank rates combined with the prospect of a weaker dollar and medium-term inflation not returning to the expected 2.5% level but instead settling around 4%. This focus was in play on Tuesday, the first proper trading day of the year, when the dollar temporarily strengthened, and bond yields dropped while stocks dropped with high profile companies like Tesla and market cap leader Apple both posting new cycle lows.

Regarding equities, our chief equity strategist Peter Garnry wrote this in a recent update: “It is a new year with fresh hopes, but all the issues around inflation, interest rates, geopolitical risks and China remain the same. In a couple of weeks from now Q4 earnings will begin to be announced and the key question is whether companies are lowering their forecasts for 2023 and continue to see headwinds on their operating margins.”

In addition to the mentioned supportive drivers for gold this year, we see continued strong demand from central banks providing a soft floor in the market. During the first three quarters of last year the World Gold Council reported official sector purchases of 673 tons, higher than any full year since 1967. Part of that demand being driven by a handful of central banks wanting to reduce their dollar exposure. This de-dollarization and general appetite for gold should ensure another strong year of official sector gold buying.

Adding to this we expect the friendlier investment environment for gold to reverse last year’s 120 tons reduction via ETF’s to a potential increase of at least 200 tons. Hedge funds meanwhile turned net buyers from early November when a triple bottom signaled a change away from the then prevailing strategy of selling gold on any signs of strength. As a result, the net position during this time flipped from a 38k contract net short to a 67k contract net long on December 27.

Traders’ conviction at the beginning of a new trading year always tends to be low for fear of catching the wrong move. At the same time, however, the fear of missing out (FOMA) can also drive a rapid buildup in positioning which subsequently can be left exposed should a change in direction occur. In the short term these mechanics will have an impact on the price action in gold, silver and platinum, not least considering their strong move higher during the first few hours of trading.

From a technical perspective the acceleration today above an already steep uptrend at $1852 has raised the risk of the market having rallied too fast too soon, and potential buyers should consider holding back waiting for a correction or consolidation phase. The next key level of resistance being the June high at $1878 followed by $1897, the latter representing the 61.8% retracement of the 2022 correction. A reversal, meanwhile, to the 21-day moving average, currently at $1802, cannot be ruled out and would signal any change in the overall positive sentiment.

Ole S Hansen is the Head of Commodity Strategy at Saxo Bank.

The opinions expressed are those of the author and may not reflect the editorial policy or an official position held by TRENDS.

{kind=link}