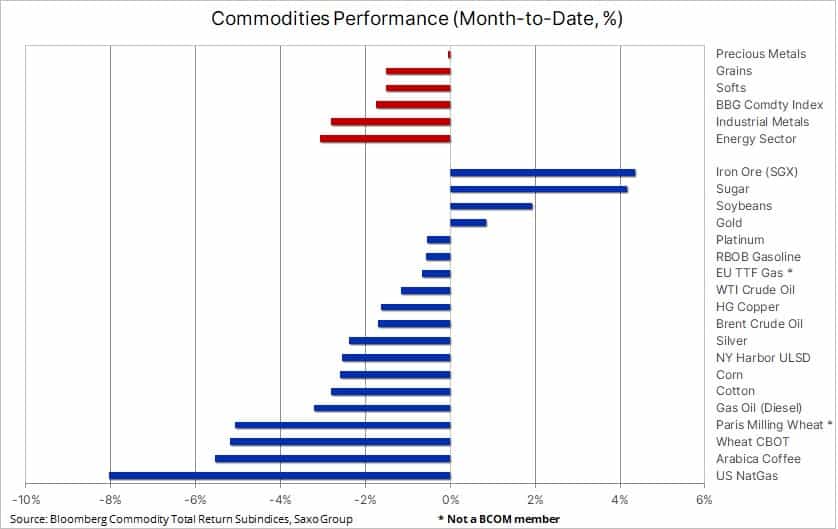

DUBAI, UAE — The month of March kicked off with continued and broad weakness after China and the US, the world’s two biggest commodity consuming nations, both delivered price softening news. Sentiment received a further setback after steep losses in two small US lenders – helping drive the S&P 500 index to a two-month low. The Bloomberg Commodity index, which tracks a broad basket of commodity futures spread evenly across energy, metals and agriculture, trades down 1.7 percent on the month and 7 percent on the year, with losses this month being led by energy and industrial metals.

The strength of the expected demand recovery in China received a setback after its leaders announced a conservative growth target of 5 percent for 2023 – one of its lowest targets in decades. This, combined with only a modest increase in fiscal support, lowered expectations for additional stimulus to accelerate the economic recovery. In Saxo’s opinion, part of the reason for this is the Chinese government’s desire to avoid making the same mistakes other governments and central banks have made, which have driven inflation to a four-decade high. Development consumers are now suffering the consequences as central banks increasingly apply their interest rate weapon to bring inflation under control.

Meanwhile, Federal Reserve Chair Powell stepped up his attack on sticky inflation. During his semi-annual two-day visit to Capitol Hill, he told lawmakers that he was prepared to increase the pace of rate hikes to a higher-than-expected level should incoming data continue to show strength. The swap market responded by lifting the terminal rate expectation above 5.66 percent from 4.75 percent at the beginning of February, before Thursday’s stock market rout across banking stocks helped bring the peak rate back down below 5.5 percent.

During the Q&A session on Tuesday that followed his prepared statement, a tasty exchange between Powell and Sen. Elizabeth Warren (D) highlighted the risk the FOMC takes as it continues to hike rates until something potentially brakes. The senator asked Powell what he will say to the two million people losing their jobs if he keeps raising rates. He answered: “Will working people be better off if we just walk away from our jobs and inflation remains 5 percent-6 percent?”.

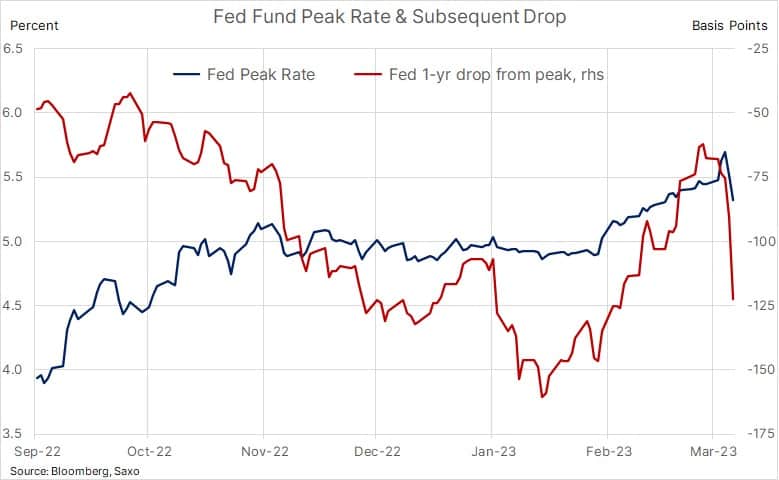

His comment further supported the view that the FOMC will remain very data driven and, besides the small risk of a systemic event taking control, it will keep hiking rates despite the obvious risk to the economic outlook. Saxo will continue to watch the dollar closely, given its inverted correlation with commodities (especially gold) and increasingly how the market price the risk of a recession and with that the scale of the eventual drop-in rates. Saxo monitors this through the terminal Fed fund expectation and the size and speed of subsequent cuts once the terminal rate is reached, currently priced to occur around September this year.

The trade stimulus from China’s reopening continued to fade, following a great deal of excitement at the start of the year, especially after the government set the mentioned moderate growth target. However, writing off China as a major driver for commodity demand growth is premature as it will take several months for the real impact to be felt and for prices to benefit. Not least considering producers tend to respond quicker in terms of adding supply before demand picks up. This was seen recently in China where a February rise in exchange monitored copper inventories has yet to be met by a corresponding pickup in demand.

Crude oil remains rangebound

The crude oil market remains rangebound with rising demand in Asia so far managing to offset darkening clouds elsewhere, especially in the US where Fed Chair Powell combatant performance on Capitol Hill this past week showed his willingness to risk a recession to bring inflation under control. While data points to a strong recovery in demand from a reopening China, the market was left disappointed after the government published the weakest growth target in decades. In addition, concerns about a banking crisis, however small, kept the risk appetite on the low side.

Overall, these on balance price negative developments, have not been enough to force the market lower and out of the ranges that have prevailed since late November. In the short-term, the macroeconomic focus is likely to override any oil market developments, unless they have a material impact on prevailing supply and demand balances. Having broken the mini uptrend within the prevailing range, Brent may in the short term be exposed to further weakness, not least driven by long liquidation from funds who in recent weeks increased their net long to a 15-month high at 286k lots or 286 million barrels. At the same time, the gross short has continued to collapse – reaching a 12 year low at just 22k lots in the week to February 28.

Gold finds support in the numbers

Gold and silver took a tumble mid-week when Fed Chair Powell, in his prepared remarks to Congress, said the Fed was prepared to increase the pace of rate hikes and to a higher-than-expected level should incoming data continued to show strength. Having failed to challenge resistance at $1864, gold tumbled before once again finding support ahead of $1800. Meanwhile, silver resumed its week-long slump, hitting a four-month low before finding some renewed buying interest around the $20 level. Relative weakness since late December has seen the gold-silver ratio surge higher from 75 (ounces of silver to one ounce of gold) to a six-month high at 91, a 21 percent underperformance, and it highlights the short-term challenge silver will be facing to attract fresh demand.

In the short-term, with Powell signalling an incredible data dependency, the focus now turns to incoming US data with the first being Friday’s job report, a number which on balance eased the pressure on the Federal Reserve to increase the size of its next rate hike, pencilled in for March 22. Given the level of elevated rate hike expectation currently priced in, any weakness in incoming data may now trigger a stronger positive response than otherwise warranted.

Saxo watches the timing of peak rates closely as well as how aggressive the market is pricing in a subsequent cut. According to the chart above, the peak rate is currently priced in around July around 5.34 percent, down from 5.70 earlier in the week. In addition, the subsequent pace of rate cuts has accelerated to 125 basis points during the following 12 months. This is important to note with gold historical performing well in the months that followed a peak in the Fed funds rate, with such a peak often being accompanied by a weaker dollar and lower bond yields.

Downside pressure on corn and wheat futures

Chicago corn and wheat futures extended their slump this week after the USDA in its monthly supply and demand update said domestic stockpiles rose by more than expected in response to lower exports. The agency also boosted the outlook for Ukraine corn exports while wheat, already under pressure from Russian sales and expectations the Ukraine grain corridor deal will be extended, dropped to a 20-month low after the agency raised production estimates for Kazakhstan, Australia and India. Meanwhile, soybeans found support after the USDA slashed production from drought-stricken Argentina by more than expected. The world’s biggest exporter of soymeal and soy oil will harvest 33 million tons of beans this year, the smallest crop since 2011 and a 20 percent decline from the agency’s February estimate.

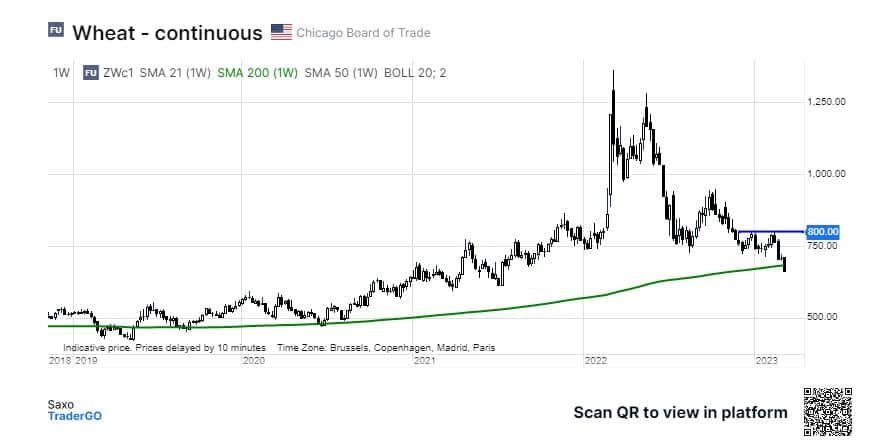

All the major wheat futures contracts in Chicago and Paris remain under pressure and, according to the relative strength indicators, they have all reached oversold territory. This is a very different story to the price action that was seen this time last year when Russia’s invasion of Ukraine – a major supplier of high protein wheat ideal for human consumption – triggered panic buying. Chicago wheat topped out at $12.85 per bushel on March 9 before suffering a 50 percent setback to the current $6.66 a bushel level.

Ole S Hansen is the Head of Commodity Strategy at Saxo Bank.

The opinions expressed are those of the author and may not reflect the editorial policy or an official position held by TRENDS.

{kind=link}