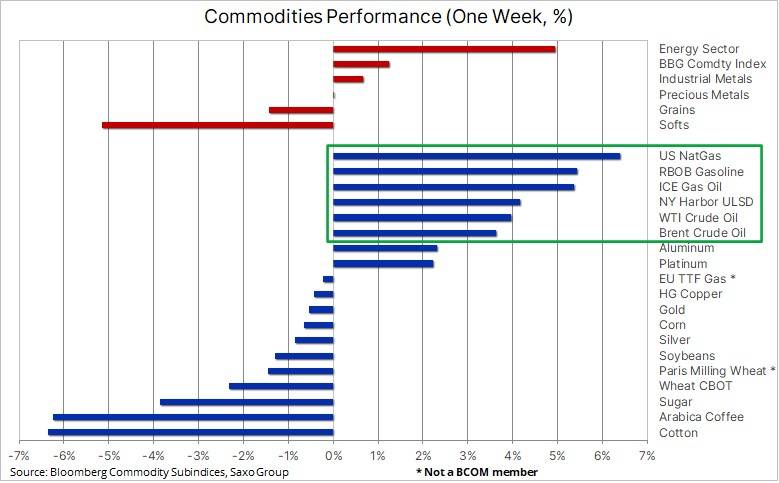

Commodities trading was mixed during this past week, with strength across the energy sector being offset by weakness in agriculture – especially the soft sector which dropped to a one-year low led by continued weakness in coffee and cotton. The industrial metal index showed a small gain, with focus on developments in China following the end of the 20th National Congress of the Chinese Communist Party, and the dollar – which traded softer on the week. Meanwhile, precious metals found some support following a change in sentiment across bonds and the dollar on speculation that we may approach peak hawkishness from the US Federal Reserve.

The latest recovery in gold followed increased speculation that the Fed is preparing to downshift in pace of rate hikes by early next year. The idea being that the FOMC’s willingness to offer time to assess the economic impact of the rapid pace of rate hikes and quantitative tightening already seen. However, some of the initial gains faded towards the end of the week after the dollar showed renewed strength especially against the euro after the ECB surprised to the dovish side, as well as the Japanese yen after the Bank of Japan maintained its yield cap and the government announced massive fiscal stimulus. With the Bank of Japan not allowing government bond yields to adjust, this risks adding to the yen’s weakness as long as other major central banks are not in easing mode.

Crude oil supported by tight fuel supply outlook

Crude oil remains on track for a second week of gains but for now without challenging resistance indicating a market still struggling for direction with no overriding theme being strong enough to set the agenda. Strength this week has been driven by a continued developing tightness in the fuel product market, US exports of crude and fuels setting a weekly record, the weaker dollar as well as strong buying from China as refineries there plan to boost fuel exports through the end of the year

While crude oil has been mostly rangebound since July, the fuel product market has continued to tighten as supplies in Europe and the US have become increasingly scarce, thereby driving up refinery margins for gasoline and distillate products such as diesel, heating oil and jet fuel. The focus in terms of tightness remains the northern hemisphere product market where low stocks of diesel and heating oil continues to raise concerns. The market has been uprooted by the war in Ukraine and sanctions against Russia, a major supplier of refined products to Europe. In addition, the high cost for gas has supported increased switching activity from gas to other fuels, especially diesel and heating oil.

This tight market situation was recently made worse by the OPEC+ decision to cut production from next month. While the continued release of US (light sweet) crude from its strategic reserves will support production of gasoline, the OPEC+ production cuts will primarily be provided by Saudi Arabia, Kuwait and the UAE – all producers of the medium/heavy crude which yields the highest amount of distillate.

As long as the product market remains this tight, the risk of seeing lower crude oil prices -despite the current worry about recession – seems to be low so we maintain our forecast for a price range in Brent for this quarter between $85 and $100, with the tightening product market increasingly skewing the risk to the upside.

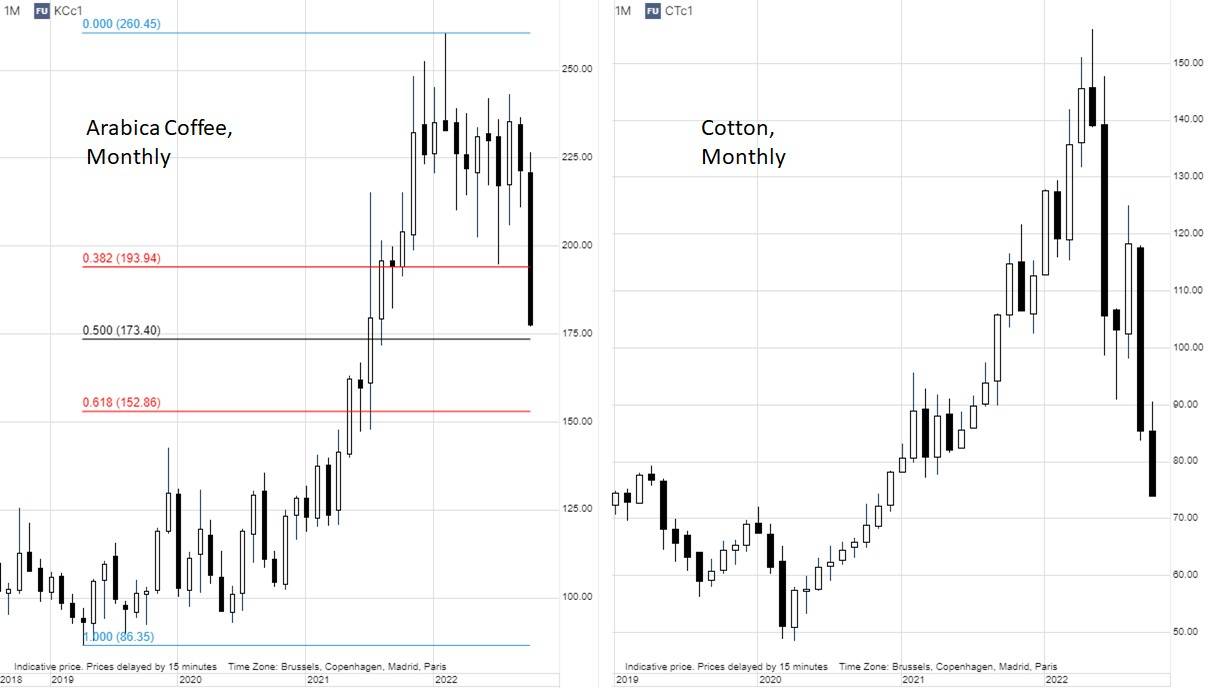

A tough period for coffee, cotton and sugar

The Bloomberg Commodity Softs index traded down 5% on the week, led by a 6% drop in Arabica coffee to 175 cents per pound. This is a 14-month low for the commodity as money managers continue to exit long-held bullish bets, which are now turning increasingly sour amid concerns that a global economic slowdown will hurt demand at a time where the outlook for the 2023/24 crop in Brazil is showing signs of improving. However, the combination of exchange monitored stocks still lingering near a 23-year low and the technical picture showing a very oversold market, could mean the market establishes some support soon – potentially around 173 cents per pound. This level would represent a 50% correction of the 2019 to 2022 rally from 86 to 260 cents.

Sugar has been hurt by a weaker Brazilian Real, which boosted incentives to export and thereby increasing supply while forcing recent established speculative longs to exit. Cotton, down 53% from its May peak has plunged to near a two-year low on weak demand for supplies as consumers around the world cut back on spending. Weekly export sales from top shipper, the US, plunged from a year earlier with overall sales for the current season being well behind last year and the long-term average. The main culprit for the slowing sales is cancellations of orders from key buyer China, as demand for textiles suffer amid the current economic slowdown. A development that is being reflected in the weakness in the MSCI World Textiles Apparel & Luxury goods index, down 35% year-to-date compared with a 22% drop in the broad MSCI World index.

Gold nervously awaits the Nov 2 FOMC meeting

At Saxo, we maintain our bullish medium but cautious short-term outlook for gold. In our latest update, we highlighted how the latest bounce has been supported by speculation that the FOMC may pause soon to assess the economic impact of the current rate hike cycle, which is currently pricing in a peak Fed funds rate just below 5% from the current 3.25%. In addition, we maintain the view that long term inflation will end up somewhere in the 4 to 5% area, well above the current market expectations for a sub 3% rate. If proven correct, it would trigger a major adjustment in breakeven and inflation swap prices – developments that may support gold through lower real yields.

Speculators and investors are likely to remain mostly side-lined until we get a clearer view on the thinking within the Federal Reserve, hence the importance of next week’s FOMC meeting. According to the weekly Commitment of Traders reports, speculators in the futures market have been whipped around for the past few weeks, thereby reducing the willingness to aggressively enter the market until a clearer picture appears. The same goes for investors in bullion-backed ETFs, who have been net sellers on an almost continued basis since June. Overall total holdings have slumped to 2965 tons to a 30-month low, down 11% from the April peak.

After once again being rejected at the key $1615 support area, gold has a minimum need to break above $1735, thereby reversing a succession of lower highs, before an end to the month-long downtrend can be called. However, the path to that level remains littered with several smaller resistance levels, especially $1687 and $1700. For now and until such time momentum can be reestablished, watch yields, geopolitical developments and the dollar for directional inspiration. The latter traded higher following the ECB and BOJ meetings, thereby reducing support for commodities – especially gold where a high negative correlation has been established in recent weeks.

Ole S Hansen is the Head of Commodity Strategy at Saxo Bank.

The opinions expressed are those of the author and may not reflect the editorial policy or an official position held by TRENDS.

{kind=link}