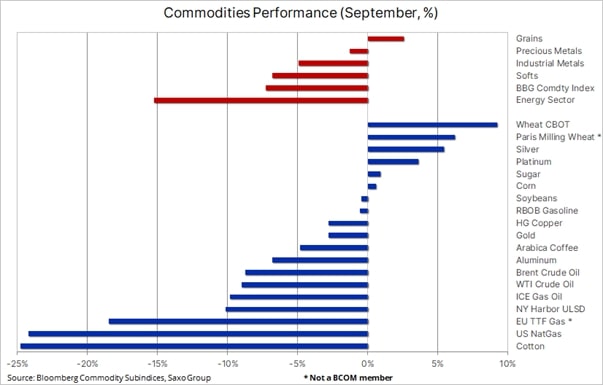

The commodity sector traded lower by around 7% in September with the weakness being driven by growth-dependent sectors, like energy and industrial metals, in response to a deteriorating outlook for global growth. This deterioration was led by China’s weakness, due to prolonged lockdowns, and Europe remaining embroiled in a historic energy crisis. Adding to this, we have witnessed a month of turmoil across financial markets driven by a surging dollar and traders sending bond yields sharply higher in anticipation of further rate hikes from central banks, led by the US Federal Reserve.

The Fed hiking into strength forcing other central banks to hike rates into weakness

While the strength of the US economy and level of inflation continues to support the hawkish approach by the US Federal Reserve, it is important to understand the impact of its actions on the global economy as several countries and regions are already witnessing a sharp slowdown. A slowdown that in many cases has been accelerated by the US exporting inflation through its rapidly appreciating currency which, together with surging Treasury yields, have put local currencies under even more strain – thereby triggering a potentially vicious circle.

With the dollar’s real effective exchange at its strongest level since 1986 and with the yield on US Treasuries surging higher, the impact on global bond markets is clear as yields rise and currencies slump – thereby creating a level of heightened instability in countries from the United Kingdom and within the European Union to China and emerging markets where rates are being hiked (although local conditions are much weaker).

All developments are rapidly driving us towards peak hawkishness in the US, from where the dollar and yields will plateau before heading lower again. However, whether something breaks before the FOMC changes its tone remains to be seen but the risk to financial stability, as seen in the UK this past week, is real and one that may impact the outlook for several commodities, especially investment metals such as gold and silver.

Commodity sector still signaling tightness despite a major correction

Multiple uncertainties, as seen through the continued level of volatility and falling liquidity, will continue to impact most commodities ahead of the year end. While the recession drums will continue to bang ever louder, the sector is unlikely to suffer a major setback before picking up speed again during 2023. The latest FOMC action and subsequent dollar strength has brought the market one step closer to peak hawkishness – which may potentially occur sometime during the final quarter of 2022. Once that happens, a subsequent peak in the dollar and Treasury yields may reduce some of the recent headwinds with the market, instead turning its focus back to multiple supply concerns.

Our forecast for stable or potentially even higher prices led by pockets of strength in key commodities across all three sectors of energy, metals and agriculture will be driven by sanctions, upstream cost inflation, adverse weather, low investment appetite and continued tightness across many key commodities from diesel and gasoline to grains and industrial metals.

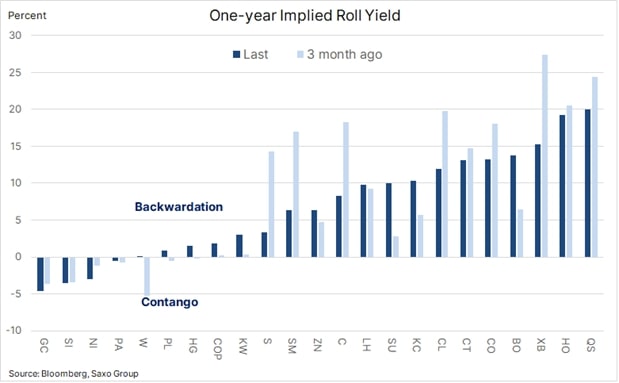

Having seen individual commodities correct from their recent peaks – by anything from 12% for key food commodities, including corn, wheat, coffee and sugar, to 77% for nickel – the heavy selling, driven by growth and demand concerns, would usually reduce the level of tightness in the market. However, looking at the spread between the front futures contract and the one expiring in 12 months, we continue to find most markets still trading in backwardation – a measure of how aggressive traders are bidding up prices to ensure immediate delivery

Gold finds a fresh bid on geopolitical risks and general market turmoil

Gold rebounded from key support at $1618, 50% retracement of the 2018 to 2020 rally, with the focus now being the critical resistance zone into 1,680-1,700 that is the departure point for this latest bear market move. While global bond yields and the USD will continue to lead the way as coincident indicators, the market has held up relatively well. Gold is being supported by geopolitical concerns – one of them being Putin’s nuclear threat – and investors are increasingly worried about the FOMC’s hawkish actions and how it may break the currency and bond market. Speculators hold a rare net short in COMEX gold futures and any further strength will trigger short covering, while total holdings in ETFs backed by bullion have declined to a 30-month low, a level from where fresh demand may emerge once the technical and/or fundamental outlook turns more friendly.

Aluminum bolts higher on Russian supply concerns

Meanwhile, silver found some relative support from a recovering industrial metal sector. This was led by a record intraday spike in aluminum after a report said the London Metal Exchange as an option was looking into whether and under what circumstances they might place a ban on Russian metal being cleared via the exchange. The sudden burst – which to a minor extent was replicated in zinc, nickel, and copper – helped lift the sector from a three-month low. Any such move by the LME to block Russian supplies could have significant ramifications for the global metal markets, given their importance together with China as a major supplier.

Having retraced a significant part of the July to August bounce, HG copper managed to reestablish some support in the $3.25 per pound area. However, at this stage, the prospect for a stronger recovery depends on the successful breakthrough of resistance beginning with $3.52 per pound and followed by $3.70 per pound.

Crude oil bears having second thoughts ahead of OPEC+ meeting

Crude oil was heading for its first (albeit small) weekly gain in five weeks but also the first quarterly drop since Q1 2020. The market remains troubled by forces, pulling prices in opposite directions. While the strong dollar, surging yields and continued lockdowns in major Chinese cities have raised demand worries, the risk to supply continues to be a supporting theme. That focus returned this week when OPEC+ said a production cut would be discussed at next week’s meeting with Russia as it proposes a 1 million barrels per day cut – a reduction towards which they are unlikely to contribute much as they are already producing below their quota. In addition, the combination of Russian sanctions, an upcoming EU embargo and price cap discussion, the US eventually pausing its sales from strategic reserves and fresh US sanctions to curb Iran’s ability to export crude oil may all continue to dampen the downside risks.

All developments that have led us to believe a low in crude oil could be found sooner rather than later with Brent then returning to a range closer to $95 than the current $85 per barrel.

Wheat on top in September driven by Ukraine export concerns

The grains sector traded higher for a second consecutive month, led by Chicago and Paris wheat – with both being supported by persistent risks of a deepening conflict in Ukraine that has put the UN-supported grain export corridor through the Black Sea at risk. Ukraine’s exports reached 0.9 million tons in August, some 2.7 million tons below last year’s pace, and that deficit may grow in September – normally the busiest month for Ukraine’s exports which reached 4.6 million tons last year.

While Russia is likely to produce a record wheat crop, Ukraine’s President Zelenskiy has warned that Russia is preparing the ground for an attempt to disrupt flows from Ukraine, another key supplier of high-quality wheat to the global market. The December wheat contract traded in Chicago traded above $9 per bushel on Friday, well below the $13.63 per bushel panic peak seen in the aftermath of Russia’s invasion but still well above the sub-$6 per bushel average seen during the last half-decade. Late on Friday after the publication of this update, the market was awaiting two key reports from the US Department of Agriculture – a quarterly stock report, which covers all major US grains, and a production update on all wheat varieties.

Ole S. Hansen is the Head of Commodity Strategy at Saxo Bank.

The opinions expressed are those of the author and may not reflect the editorial policy or an official position held by TRENDS.

{kind=link}